Agentic Digital Finance = AgenticDfin |

|

| Robotic Process Automation + Artificial Intelligence = Intelligent Automation |

|

BofI Build Very Detail Banking In Detail PDF |

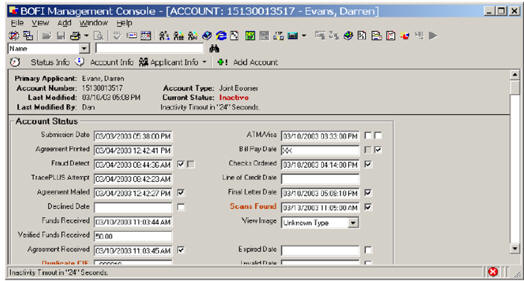

The Genesis of BofI: Example From Year 2000 |

The AgenticDfin Bank Build Process |

Ai Staff Training Example Talk With Evans Imagine Training Staff This way.  |

Video Presentation - History of Bank Technology

|

|

DFIN, BofI and The Evolution of BankingUsing RPA in 2000

|

Exhibit A – 2026

Skip Trace Data Fields in 2026

The following are the most effective

data fields and techniques used by banking skip tracers to

locate individuals. This has many more fields than I used

in the past. 1 - Core Identity & Contact Fields These fields serve as the foundation

for any trace, helping to differentiate the subject from

others with similar names.

2 - High-Yield Location Fields Banks prioritize "Right-Party Contact"

(RPC) by looking for the most recently reported physical

locations.

3 - Employment & Financial

Intelligence Locating a workplace is often more

effective than a home address for establishing contact or

executing legal remedies.

4 - Advanced Associative Fields When direct leads go cold, banks use

"linking" data to find the individual through their network.

|

Exhibit B

Robotic Process Automation

"Robotic Process Automation" was

first coined and entered the press in the early 2000s.

·

Early 2000s: Industry

pioneers like Blue Prism first released early RPA software

products around 2003.

·

2012: This was the

pivotal "breakout year" when the term achieved widespread

enterprise press and media coverage. Major outlets began

running prominent feature pieces, such as The Economist

publishing its highly cited "Rise of the software machines"

article. |